.png)

Why Consider Whole Life Insurance for Final Expenses

- Lincoln De Freitas

- Jan 4

- 10 min read

Over 60 percent of Canadian seniors place financial security for their families above all else when planning for final expenses. Facing the reality of end-of-life costs, many individuals worry about leaving behind unexpected bills or burdens. Whole life insurance stands out as a solution that goes beyond what typical American term policies offer, providing stable lifelong coverage and a built-in financial asset. This guide breaks down how whole life insurance can protect your loved ones and bring lasting peace of mind.

Table of Contents

Key Takeaways

Point | Details |

Whole Life Insurance Provides Lifelong Coverage | Whole life insurance offers permanent protection with fixed premiums and a guaranteed death benefit for seniors. |

Cash Value Offers Financial Flexibility | The cash value component grows tax-deferred and can be utilized for loans or withdrawals, enhancing financial planning options. |

Understanding Policy Types is Crucial | Different whole life insurance types cater to various health needs and coverage requirements; seniors should compare options carefully. |

Avoid Common Selection Mistakes | Seniors should assess coverage needs comprehensively and consult with professionals to ensure optimal policy selection and avoid underinsurance. |

Whole Life Insurance Defined for Seniors

Whole life insurance represents a permanent insurance solution designed specifically for seniors seeking lifelong financial protection and predictable coverage. Unlike term life policies that expire after a set period, whole life insurance provides guaranteed coverage that remains active until the policyholder passes away, as long as premiums continue to be paid consistently.

The core characteristics of whole life insurance for seniors include fixed premium rates, a guaranteed death benefit, and a unique cash value component that accumulates over time. This cash value grows tax-deferred and can be borrowed against or used to supplement retirement income. Seniors find this feature particularly attractive because it offers financial flexibility beyond traditional life insurance protection. Many policies allow partial withdrawals from the accumulated cash value without completely surrendering the policy.

A key advantage for seniors is the policy’s ability to cover final expenses, which can include funeral costs, outstanding medical bills, and potential estate settlement fees. These policies typically provide between $5,000 to $50,000 in coverage, allowing families to avoid unexpected financial burdens during an already difficult emotional period. The premiums remain consistent throughout the policyholder’s lifetime, providing predictability and peace of mind.

Structurally, whole life insurance differs from other insurance types by building equity through its cash value component. Premiums are divided between maintaining the death benefit and contributing to the policy’s investment aspect. This means that as you age, your policy becomes more than just protection - it transforms into a potential financial asset that can provide additional support during retirement years.

Pro tip: When considering whole life insurance, request illustrations comparing different coverage amounts and carefully review the guaranteed versus projected cash value to make the most informed decision.

Types of Whole Life Policies Explained

Whole life insurance offers multiple specialized policy types designed to meet the unique needs of seniors seeking comprehensive financial protection. The most common variants include traditional whole life, guaranteed issue, and simplified issue policies, each with distinct features tailored to different health circumstances and coverage requirements.

Traditional whole life insurance represents the standard option, requiring a comprehensive medical examination and offering the most competitive premium rates. These policies provide full medical underwriting through comprehensive financial services that evaluate an individual’s complete health profile. Seniors in good health can secure substantial coverage with lower monthly premiums, making this an attractive option for those with clean medical records and no significant health complications.

Guaranteed issue whole life policies offer a critical alternative for seniors with pre-existing medical conditions or those who might not qualify for traditional coverage. These policies provide guaranteed acceptance without medical examinations, though they typically come with higher premium costs and lower initial coverage amounts. The key advantage is accessibility - no one can be denied coverage based on health status, providing a lifeline for individuals who might otherwise struggle to obtain life insurance protection.

Simplified issue whole life insurance strikes a balance between traditional and guaranteed issue policies. These policies require a brief health questionnaire but do not mandate a full medical exam. They offer moderate coverage amounts with more reasonable premiums compared to guaranteed issue policies, making them an attractive middle-ground option for seniors with minor health concerns who do not qualify for the most competitive traditional rates.

Here’s a concise comparison of the main types of whole life insurance policies for seniors:

Policy Type | Medical Requirement | Typical Coverage Amount | Premium Characteristics |

Traditional | Full medical exam required | Higher, flexible | Lowest rates for healthy individuals |

Guaranteed Issue | No medical exam, no denial | Lower, limited | Highest rates due to poorer health risk |

Simplified Issue | Short health questionnaire | Moderate, balanced | Mid-range rates, easier qualification |

Pro tip: Compare multiple policy types and request personalized quotes to understand how different whole life insurance options align with your specific health profile and financial goals.

How Whole Life Insurance Works for Final Expenses

Whole life insurance serves as a strategic financial tool specifically designed to manage end-of-life expenses, offering seniors a comprehensive solution for protecting their families from unexpected financial burdens. Comprehensive final expense coverage typically ranges between $5,000 and $50,000, providing a dedicated financial safety net for funeral costs, outstanding medical bills, and potential estate settlement expenses.

The mechanics of whole life insurance for final expenses involve a unique dual-purpose structure. Premiums are divided into two primary components: maintaining the guaranteed death benefit and building a tax-deferred cash value that grows over time. Whole life insurance provides a guaranteed death benefit for your entire lifetime, ensuring that beneficiaries receive a predetermined payout regardless of when the policyholder passes away. This predictability offers families critical financial protection and peace of mind during emotionally challenging times.

Unlike term life insurance, whole life policies designed for final expenses maintain consistent premium rates throughout the policyholder’s lifetime. The cash value component allows seniors to potentially borrow against the policy or use accumulated funds to supplement retirement income. Some policies even offer dividend payments, which can be used to reduce premiums or enhance the overall policy value. This flexibility makes whole life insurance a versatile financial planning tool that extends beyond simple end-of-life expense coverage.

The payout process for final expense policies is typically straightforward and rapid. Beneficiaries can usually receive funds within days of submitting necessary documentation, allowing immediate access to resources for funeral arrangements, debt settlement, and other urgent financial needs. The streamlined claims process helps families focus on grieving and healing rather than navigating complex financial challenges during a difficult transition.

Pro tip: Request a detailed policy illustration that breaks down premium allocation, projected cash value growth, and potential dividend scenarios to fully understand your whole life insurance investment.

Key Features: Lifelong Coverage and Cash Value

Whole life insurance stands out for its lifelong coverage, a critical feature that provides seniors with permanent financial protection beyond traditional term life policies. Comprehensive insurance solutions ensure that beneficiaries receive a guaranteed death benefit regardless of when the policyholder passes away, offering unparalleled peace of mind and financial security for families.

The cash value component represents another unique aspect of whole life insurance that sets it apart from other insurance products. This feature allows policyholders to accumulate a tax-deferred savings element that grows steadily over time. Seniors can leverage this cash value through partial withdrawals or policy loans, providing a flexible financial tool that serves multiple purposes. The cash value acts as a living benefit, enabling policyholders to access funds for unexpected expenses, supplement retirement income, or address urgent financial needs without completely surrendering the policy.

Lifelong coverage means premiums remain fixed throughout the policyholder’s lifetime, creating predictability and stability in financial planning. Unlike term life insurance that expires after a set period, whole life policies provide continuous protection that adapts to changing life circumstances. The guaranteed death benefit ensures that families receive financial support, covering final expenses, outstanding debts, and potential estate settlement costs without the uncertainty of policy expiration.

The accumulation of cash value follows a structured approach, with a portion of each premium contributing to the policy’s investment component. This gradual growth occurs on a tax-deferred basis, allowing seniors to build a financial resource that can be strategically used during retirement years. Some policies even offer potential dividend payments, further enhancing the policy’s overall value and providing additional financial flexibility.

Below is a summary highlighting how coverage and cash value features impact seniors:

Feature | Description | Impact on Seniors |

Lifelong Coverage | Permanent protection until death | Provides lifelong financial security |

Fixed Premiums | Unchanging payments for duration | Predictable budgeting in retirement |

Cash Value | Grows tax-deferred, usable funds | Flexibility for loans and withdrawals |

Pro tip: Request a comprehensive policy illustration that details the projected cash value growth and potential loan options to fully understand the long-term financial benefits of your whole life insurance investment.

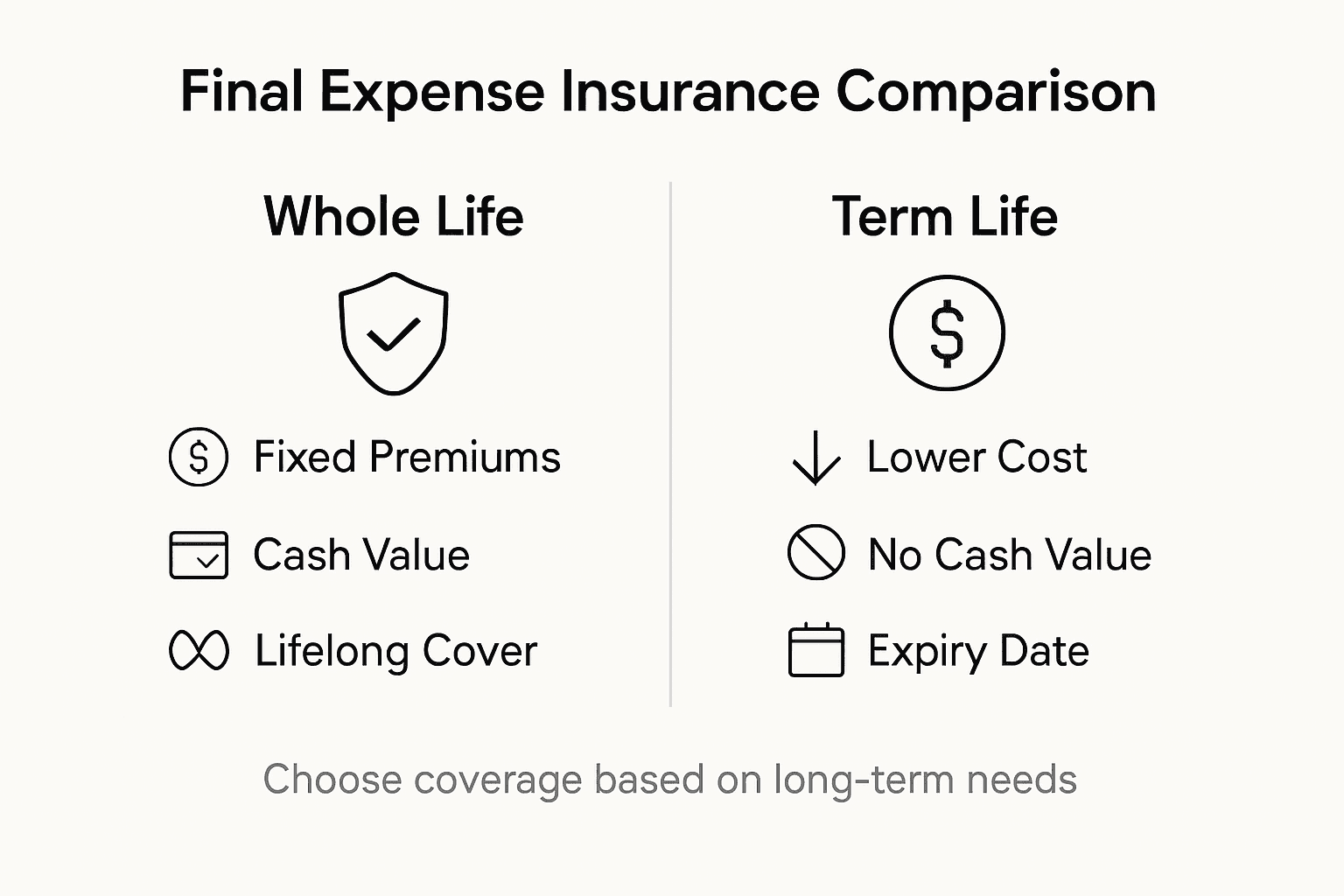

Cost Comparison With Term and Guaranteed Issue

Understanding the cost differences between whole life, term life, and guaranteed issue policies is crucial for seniors seeking the most appropriate financial protection. Cost structures vary significantly across different insurance types, with each option presenting unique financial implications for individuals in different health and financial circumstances.

Term life insurance emerges as the most budget-friendly option, offering lower initial premiums but limited coverage duration. In contrast, whole life insurance provides lifelong protection with higher premium rates that remain consistent throughout the policyholder’s lifetime. Guaranteed issue policies represent a specialized solution for seniors with health challenges, typically featuring the highest premium rates and more restrictive coverage limits due to their no-medical-exam accessibility.

The cost breakdown reveals nuanced differences that seniors must carefully consider. Term life policies might start at 30-70% lower monthly premiums compared to whole life insurance, but they lack the cash value accumulation and permanent coverage. Whole life insurance premiums are substantially higher but include the added benefit of a growing cash value component and guaranteed lifelong protection. Guaranteed issue policies often come with the steepest pricing, reflecting the increased risk assumed by insurers when providing coverage without comprehensive health screenings.

Seniors should evaluate their specific financial situation, health status, and long-term protection needs when comparing these insurance options. While term life appears most affordable initially, whole life insurance offers more comprehensive protection and financial flexibility. Guaranteed issue policies provide a critical safety net for those who might not qualify for traditional coverage, albeit at a higher cost. The key is balancing immediate budget constraints with long-term financial security and protection for loved ones.

Pro tip: Request multiple quotes from different insurance providers and carefully compare the total lifetime cost, not just the initial premium rates, to make the most informed decision.

Mistakes to Avoid When Choosing Your Policy

Selecting the right whole life insurance policy requires careful consideration and avoiding common pitfalls that can compromise your financial protection. Final expense insurance strategies demand a strategic approach to prevent potentially costly mistakes that could leave your family vulnerable during challenging times.

Underestimating Coverage Needs represents one of the most significant errors seniors make. Many individuals choose insufficient coverage amounts based on current expenses, failing to account for potential future medical costs, inflation, and unexpected financial obligations. Seniors should conduct a comprehensive assessment of total potential expenses, including outstanding debts, funeral costs, medical bills, and potential estate settlement fees. Calculating a coverage amount that provides a financial buffer beyond immediate needs ensures comprehensive protection for loved ones.

Another critical mistake involves overlooking the importance of the cash value component and policy flexibility. Some seniors select policies without fully understanding how the cash value accumulates or the potential loan and withdrawal options. This can lead to missed opportunities for financial flexibility during retirement years. Additionally, failing to review policy details such as premium payment structures, potential dividend options, and long-term growth projections can result in unexpected financial limitations. Seniors should request detailed policy illustrations and carefully examine how different policy features align with their specific financial goals and retirement planning strategies.

Procrastination and avoiding medical underwriting can also prove detrimental to securing optimal insurance coverage. Waiting too long to purchase a policy typically results in significantly higher premiums and potentially limited coverage options. Younger, healthier seniors can secure more comprehensive coverage at more competitive rates, making early planning crucial. Moreover, some individuals mistakenly choose guaranteed issue policies without exploring other options, potentially paying substantially higher premiums when they might qualify for more affordable traditional whole life insurance with medical underwriting.

Pro tip: Consult with a licensed insurance professional who specializes in senior life insurance to conduct a personalized policy review and identify the most suitable coverage for your unique financial situation.

Secure Your Family’s Future with Whole Life Insurance for Final Expenses

Facing the challenge of covering final expenses can be overwhelming. The article highlights the importance of predictable, lifelong coverage with features like guaranteed death benefits and cash value growth. You deserve peace of mind knowing that funeral costs, outstanding medical bills, and estate fees will not become a financial burden for your loved ones. Understanding the differences between traditional, guaranteed issue, and simplified issue policies helps you make an informed choice tailored to your health and budget.

At LD Financial Services, we specialize in compassionate and transparent final expense insurance solutions designed especially for seniors. Our licensed agents guide you through simplified application processes and fixed premiums, ensuring you find the right coverage that protects your legacy while easing your family’s future financial stress.

Take the first step towards lifelong security today

Explore options that fit your unique situation by visiting LD Financial Services. Book a personalized consultation and learn how our guaranteed issue life insurance and whole life insurance plans can provide affordable, enduring protection for those final expenses. Act now so your family is protected when it matters most.

Frequently Asked Questions

What is whole life insurance for final expenses?

Whole life insurance for final expenses is a permanent life insurance policy designed to provide financial coverage for end-of-life costs such as funeral expenses, medical bills, and estate settlement fees. It offers guaranteed coverage throughout the policyholder’s lifetime as long as premiums are paid.

How does whole life insurance accumulate cash value?

Whole life insurance policies include a cash value component that grows tax-deferred over time. A portion of the premiums paid contributes to this cash value, which can be borrowed against or withdrawn to supplement retirement income or cover unexpected expenses.

Why is whole life insurance preferred for final expenses?

Whole life insurance is preferred for final expenses because it offers a guaranteed death benefit, fixed premiums for life, and a cash value that can help alleviate the financial burden on families during a difficult emotional period. It ensures that loved ones receive financial support without worrying about unexpected costs.

What types of whole life insurance policies are available for seniors?

Seniors can choose from several types of whole life insurance policies, including traditional whole life, guaranteed issue, and simplified issue policies. Each type has different eligibility requirements, coverage amounts, and premium structures, catering to various health conditions and financial needs.

Recommended