.png)

Term Life Insurance: Protecting Family and Legacy

- Lincoln De Freitas

- 5 days ago

- 8 min read

More than 40 percent of American and Canadian families lack adequate life insurance to secure financial stability. For adults aged 50 to 70, protecting loved ones from end-of-life expenses is a serious concern that often leads to difficult choices. Understanding term life insurance gives you the clarity to select affordable coverage that matches your needs. This guide cuts through confusion and spotlights options designed to protect your family’s future without straining your budget.

Table of Contents

Key Takeaways

Point | Details |

Understanding Term Life Insurance | Term life insurance provides financial protection for families during critical life stages for a specific period, with premiums based on age and health. |

Types of Policies | Two main types exist: level term, which maintains a constant death benefit, and decreasing term, which lowers the benefit over time as obligations decrease. |

Eligibility and Application | Qualifying involves an assessment of health and lifestyle factors, with honesty in the application crucial to ensure policy validity. |

Cost Insights | Premiums vary based on individual risk factors and understanding payout conditions is essential, as benefits only apply if death occurs during the policy term. |

What Term Life Insurance Really Means

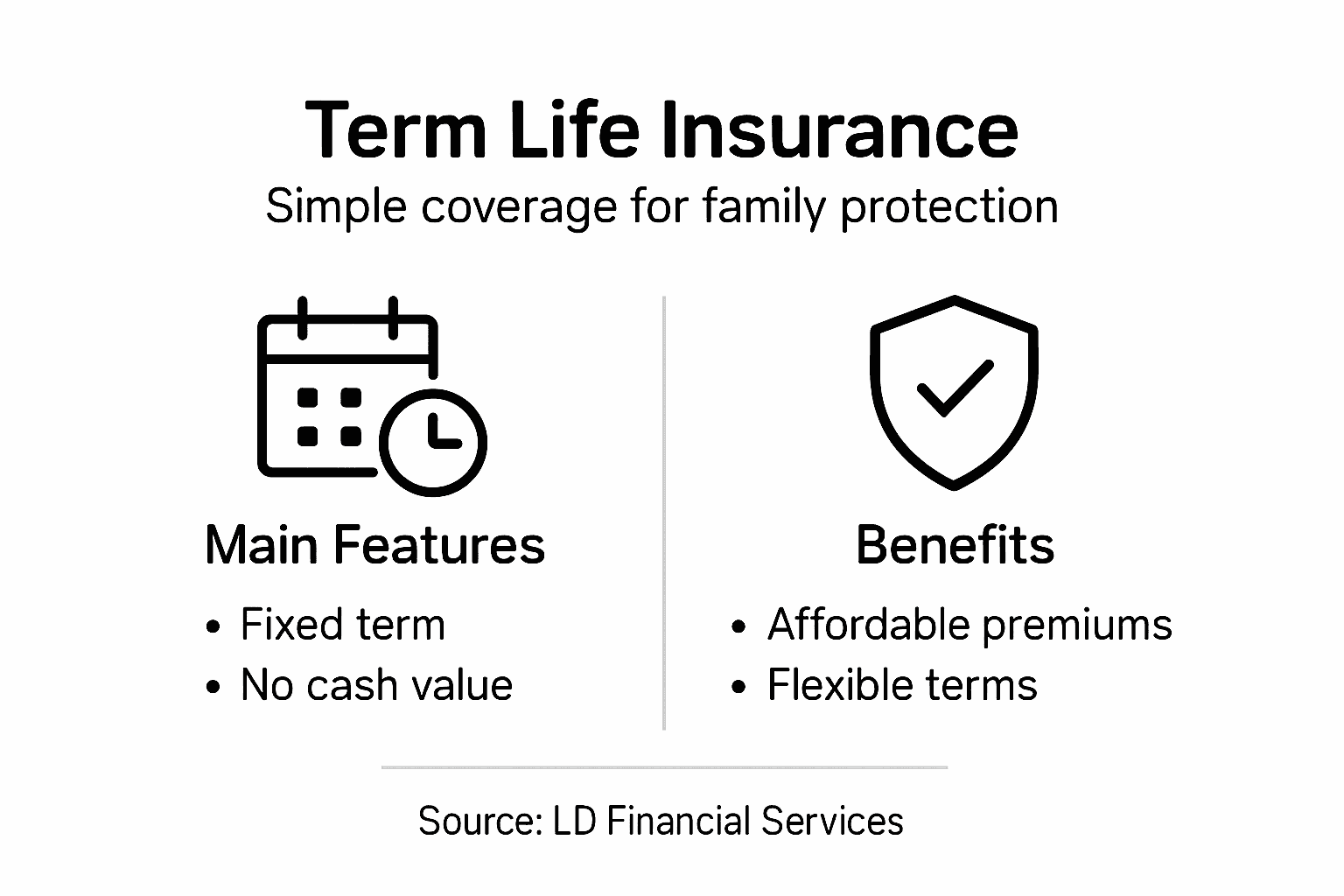

Term life insurance is a straightforward financial protection strategy designed specifically for families seeking temporary yet substantial coverage during critical life stages. Unlike permanent insurance options, term policies provide coverage for specific time periods with clear, predictable parameters.

At its core, term life insurance operates on a simple principle: you pay regular premiums for a predetermined period, typically ranging from 10 to 30 years, and if you pass away during that timeframe, your designated beneficiaries receive a predetermined death benefit. These policies are particularly attractive for individuals with specific financial responsibilities like mortgage payments, dependent care costs, or children’s education expenses. The coverage amount can be strategically selected to match anticipated financial needs, ensuring your family remains financially secure even in your absence.

The mechanics of term life insurance are relatively straightforward. When you purchase a policy, you select a coverage amount and term length that aligns with your family’s potential financial vulnerabilities. Premiums are structured based on age, health, and coverage amount, with younger, healthier individuals typically receiving more affordable rates. Once the term expires, the policy terminates unless you choose to renew or convert it. This flexibility makes term life insurance an adaptable tool for managing financial risk during key life transitions.

Pro tip: Before selecting a term life insurance policy, carefully assess your family’s long-term financial needs and choose a coverage amount that provides comprehensive protection without overextending your budget.

Types of Term Life Policies Explained

Term life insurance offers several distinct policy types, each designed to meet different financial protection needs. Policies typically come in two primary variations: level term and decreasing term, each with unique characteristics that can align with specific family financial strategies.

Level term policies represent the most common and straightforward option. In these policies, the death benefit remains constant throughout the entire term, providing predictable financial protection. The coverage amount stays the same whether you’re in the first or final year of the policy, making it ideal for families with consistent long-term financial obligations like mortgage payments or children’s education expenses. These policies typically offer term lengths ranging from 10 to 30 years, allowing individuals to choose coverage that matches their anticipated financial responsibilities.

Decreasing term policies take a different approach, with the death benefit gradually reducing over time, usually in alignment with declining financial obligations. These policies can be structured with varying premium and benefit configurations, making them particularly suitable for scenarios like mortgage protection where outstanding debt diminishes over time. Some policies also offer additional flexibility, such as renewable terms or conversion options to permanent life insurance without requiring new medical examinations.

Pro tip: Carefully evaluate your family’s specific financial trajectory and potential future obligations when selecting between level and decreasing term life insurance policies to ensure the most appropriate coverage.

Here’s a quick comparison of the main types of term life insurance policies:

Policy Type | Death Benefit Trend | Best Used For | Typical Term Length |

Level Term | Remains constant | Long-term debts, education expenses | 10 to 30 years |

Decreasing Term | Reduces over time | Mortgage protection, declining debts | 10 to 30 years |

Key Features and How Coverage Works

Term life insurance provides a straightforward approach to financial protection, designed to cover specific financial responsibilities during critical life periods. Unlike permanent life insurance, this type of policy focuses on providing a precise safety net for your family during predetermined timeframes when financial vulnerability is most acute.

The fundamental mechanics of term life insurance revolve around three core components: the coverage amount, the term length, and the premium structure. Policyholders select a death benefit that reflects their family’s potential financial needs, choosing term lengths typically ranging from 10 to 30 years. Premiums are generally fixed throughout the selected term, allowing for predictable financial planning. The policy remains active as long as premium payments are maintained, providing a guaranteed death benefit to beneficiaries if the insured passes away during the specified term.

One critical aspect of term life insurance is its lack of cash value accumulation. Unlike whole life policies, term life focuses exclusively on providing pure death benefit protection without building investment components. This design allows for more affordable premiums, making it an attractive option for individuals seeking maximum coverage at minimal cost. Most policies offer additional flexibility, such as the ability to convert to permanent insurance or renew coverage, though these options may come with adjusted premium rates.

Pro tip: Calculate your ideal coverage amount by multiplying your annual income by the number of years your family would need financial support, then add any significant outstanding debts to determine the most appropriate term life insurance protection.

Eligibility and Application Process Details

Qualifying for term life insurance requires navigating a comprehensive assessment of personal health and lifestyle factors. Insurance providers evaluate multiple dimensions of an applicant’s profile to determine coverage eligibility, premium rates, and potential risk. Age, health history, occupation, and lifestyle choices all play crucial roles in this intricate evaluation process.

The application journey typically involves several detailed steps. Applicants must complete an extensive form providing comprehensive personal and medical information, which becomes the foundation for the insurance company’s risk assessment. Underwriting processes examine medical records, lifestyle factors, and potential health risks to determine coverage parameters. Most applications require a medical examination, which might include blood tests, medical history review, and potential physician statements. Factors such as chronic conditions, high-risk occupations, or dangerous hobbies can significantly impact both eligibility and premium calculations.

Different term life insurance policies offer varying application complexity. Some group policies provide simplified processes with minimal medical scrutiny, while individual policies demand more rigorous health evaluations. Applicants should prepare detailed documentation including medical history, current health status, family medical background, prescription records, and lifestyle information. Honesty is paramount during this process, as any misrepresentation could potentially invalidate the entire policy or create complications during future claim processes.

Pro tip: Before applying, collect all medical records, prepare a comprehensive list of medications, and schedule a comprehensive physical examination to increase your chances of securing favorable coverage terms.

This overview summarizes the key factors affecting term life insurance costs and eligibility:

Factor | Influence on Cost | Impact on Eligibility | Typical Assessment Method |

Age | Higher age increases premiums | Older age may limit eligibility | Verified via applicant records |

Health History | Chronic conditions raise costs | Serious issues may cause denial | Medical exam and review |

Coverage Amount | Higher amount raises premiums | Larger policies require stricter review | Set by applicant, reviewed by insurer |

Lifestyle Choices | Risky habits increase cost | High-risk choices may result in rejection | Lifestyle questionnaire |

Costs, Payouts, and Common Misconceptions

Term life insurance represents an affordable approach to financial protection, with costs primarily determined by individual risk factors. Premium calculations incorporate multiple variables including age, health status, lifestyle choices, and desired coverage amount. Younger, healthier applicants typically secure more competitive rates, while older individuals or those with complex medical histories may face higher premium structures.

The payout mechanism of term life insurance is straightforward yet critical to understand. Payouts occur exclusively when death happens during the specified policy term, with no benefit if the policyholder outlives the coverage period. This fundamental characteristic often surprises individuals who mistakenly believe they will receive funds regardless of survival. Some policies offer return of premium options, but these come with significantly higher initial costs and should be carefully evaluated against standard term policies.

Numerous misconceptions surround term life insurance that can lead to poor financial planning decisions. Many people incorrectly assume premiums remain constant throughout life or that these policies build cash value like permanent insurance products. In reality, term policies are designed as pure protection mechanisms, focusing exclusively on providing financial security for beneficiaries during specific vulnerable periods. The temporary nature of coverage allows for more affordable premiums compared to permanent life insurance, making it an attractive option for individuals seeking targeted financial protection.

Pro tip: Compare multiple insurance quotes from different providers, and carefully review the specific terms, exclusions, and conversion options to ensure you select a term life policy that genuinely matches your family’s long-term financial protection needs.

Secure Your Family’s Future with Trusted Term Life Insurance

Understanding term life insurance is the first step toward protecting your loved ones during life’s uncertain moments. If you worry about leaving behind unpaid debts, funeral expenses, or other financial burdens, you are not alone. The key challenges are choosing the right coverage amount and term length to match your family’s needs while ensuring affordable premiums and straightforward application processes.

At LD Financial Services, we focus on compassionate and transparent life insurance solutions tailored for individuals planning their financial legacy. Whether you seek a pure term life policy or want to explore options including guaranteed issue or permanent insurance, our licensed agents simplify the process and help you avoid costly mistakes. We know that securing your family’s financial future matters now more than ever.

Take control today by visiting Our Home Page.

Don’t wait to make decisions about critical end-of-life costs. Connect with an expert at LD Financial Services now to get fast, affordable term life insurance quotes designed for your unique situation. Protect your family and ensure peace of mind with coverage that fits your budget and goals.

Frequently Asked Questions

What is term life insurance?

Term life insurance is a temporary financial protection strategy that provides coverage for a specific period, typically between 10 to 30 years. If the insured passes away during this term, the beneficiaries receive a predetermined death benefit.

How do level term and decreasing term life insurance policies differ?

Level term policies maintain a constant death benefit throughout the term, making them ideal for ongoing financial obligations. Decreasing term policies feature a death benefit that gradually reduces over time, which is often aligned with decreasing debts, like a mortgage.

What factors influence the cost of term life insurance premiums?

The cost of term life insurance is determined by several factors, including the applicant’s age, health, lifestyle choices, and the coverage amount selected. Generally, younger and healthier individuals can secure more affordable rates.

Can term life insurance accumulate cash value like permanent insurance?

No, term life insurance does not accumulate cash value. It is designed solely for death benefit protection without investment components, allowing for lower premiums compared to permanent life insurance options.

Recommended