.png)

End-of-Life Expenses – How They Impact Your Legacy

- Lincoln De Freitas

- Dec 16, 2025

- 9 min read

Over half of American families encounter unexpected costs during end-of-life transitions, often discovering that medical bills only make up a fraction of the total financial burden. This can be a shocking realization for those who assume insurance will cover everything, leaving families to sort through funeral fees, legal paperwork, and outstanding debts on short notice. By understanding the real scope of these expenses and seeing through common myths, you can make decisions that truly protect both your legacy and your loved ones.

Table of Contents

Key Takeaways

Point | Details |

Understand End-of-Life Expenses | End-of-life expenses extend beyond medical costs and include funeral arrangements, legal fees, and outstanding debts, significantly impacting financial planning. |

Debunk Common Myths | Many mistakenly believe that healthcare costs dominate the final year of life, but only 13% of healthcare spending occurs then, emphasizing the need for comprehensive planning. |

Implement Proactive Financial Strategies | Creating an end-of-life expense fund and documenting financial preferences at least 3-5 years before retirement can ease the burden on surviving family members. |

Explore Insurance Options | Final expense insurance provides a way to cover essential costs without the complexities of traditional life insurance, allowing for more straightforward planning. |

Defining End-of-Life Expenses and Common Myths

End-of-life expenses are financial obligations that arise during an individual’s final stage of life, encompassing medical care, funeral arrangements, legal documentation, and potential outstanding debts. These costs can significantly impact a person’s legacy and financial planning, often surprising families who are unprepared for the comprehensive financial burden associated with end-of-life transitions.

Contrary to popular belief, end-of-life expenses are not exclusively medical. Recent research challenges the myth that healthcare spending is predominantly concentrated in a person’s final year, revealing that only 13% of personal healthcare expenditures occur during an individual’s last year of life. This statistic underscores the importance of understanding the broader spectrum of end-of-life financial considerations beyond immediate medical costs.

Common myths surrounding end-of-life expenses can lead to inadequate financial preparation. Many individuals mistakenly assume that standard health insurance or government programs will cover all necessary expenses. Harvard Health highlights several misconceptions about end-of-life care, including the belief that more medical intervention is always beneficial and that refusing life support equates to giving up. These myths can complicate personal and familial decision-making processes.

Understanding the true nature of end-of-life expenses requires a holistic approach that considers medical costs, funeral expenses, potential legal fees, outstanding debts, and the financial impact on surviving family members. By dispelling common myths and proactively planning, individuals can create a more comprehensive strategy that protects their legacy and provides financial peace of mind.

Pro Tip: Financial Preparation Insight: Start documenting and discussing your end-of-life financial preferences with trusted family members at least 3-5 years before retirement to ensure a smoother, less stressful transition for everyone involved.

Main Categories of End-of-Life Costs

End-of-life expenses encompass a complex array of financial obligations that extend far beyond simple medical treatments. These costs typically fall into several critical categories that can quickly accumulate and create significant financial strain for families during an already challenging time. Understanding these categories helps individuals and families develop more comprehensive financial planning strategies.

Medical Expenses represent the most substantial component of end-of-life costs. Research examining healthcare expenditures reveals that inpatient admissions account for nearly 80% of total expenses in an individual’s final year. These medical costs can include hospital stays, specialized treatments, medication, medical equipment, nursing care, and potential long-term care services. Unplanned hospital care, in particular, can constitute a significant portion of these expenses, often creating unexpected financial burdens.

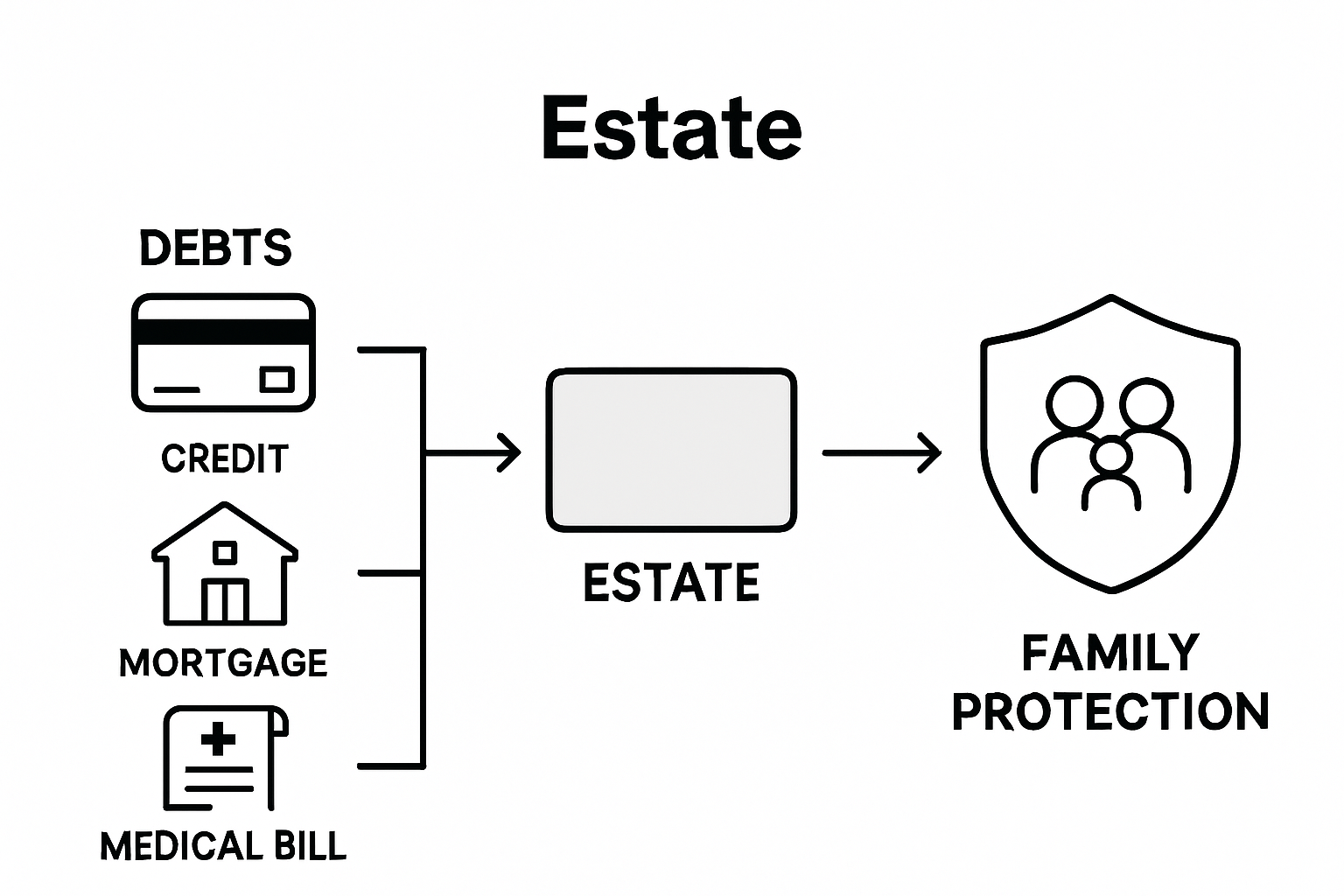

Beyond medical expenses, end-of-life costs also encompass several other critical financial categories. Funeral and Burial Expenses can range from several thousand to tens of thousands of dollars, including funeral service fees, casket or cremation costs, burial plot expenses, and memorial service arrangements. Legal and Administrative Costs include expenses related to estate planning, will preparation, probate processes, and potential legal consultations. Outstanding Debt Settlements are another crucial consideration, as remaining credit card balances, mortgage payments, personal loans, and other financial obligations do not automatically disappear upon an individual’s passing.

The complexity of these expenses underscores the importance of proactive financial planning. Additional research highlights that unplanned hospital care represents 57% of additional end-of-life expenses, emphasizing the need for comprehensive financial strategies that anticipate potential medical and non-medical costs.

Here’s a summary comparison of the main categories of end-of-life expenses and their typical financial impact:

Expense Category | Typical Cost Range | Key Challenges |

Medical Expenses | $10,000 to $100,000+ | Unplanned hospital care, limited coverage |

Funeral & Burial Costs | $7,000 to $12,000 | Rapid decisions, emotional spending |

Legal/Administrative | $500 to $5,000+ | Probate fees, will and estate issues |

Outstanding Debt | Variable, unlimited | Creditor claims, family liability risks |

Pro Tip: Financial Preparation Strategy: Create a dedicated end-of-life expense fund at least 5-10 years before retirement, allocating resources specifically for potential medical, funeral, and administrative costs to reduce financial stress on your family.

How Final Expense Insurance Works

Final expense insurance represents a specialized financial tool designed to address the unique challenges of end-of-life financial planning. This targeted insurance product offers a streamlined approach to covering funeral expenses, medical bills, and other essential end-of-life costs, providing families with critical financial protection during emotionally challenging times.

How It Functions: Final expense insurance operates as a type of whole life insurance with specific characteristics tailored to seniors and individuals seeking modest coverage. Unlike traditional life insurance policies with extensive death benefits, these policies typically offer smaller monetary amounts ranging from $5,000 to $35,000. The primary purpose is to ensure immediate financial resources are available to cover funeral expenses, outstanding medical bills, and other critical end-of-life financial obligations without burdening surviving family members.

The application process for final expense insurance differs significantly from traditional life insurance. Most policies feature simplified underwriting, meaning applicants can often qualify without comprehensive medical examinations. This accessibility makes these policies particularly attractive for older adults or individuals with pre-existing health conditions who might struggle to obtain standard life insurance coverage. Premiums remain fixed throughout the policy’s duration, providing predictable financial planning and eliminating concerns about escalating insurance costs.

Key considerations for potential policyholders include understanding the specific coverage limits, evaluating the policy’s payout structure, and confirming the absence of waiting periods that might restrict immediate benefits. Beneficiaries typically receive funds quickly, allowing them to address funeral arrangements and immediate financial responsibilities without significant bureaucratic delays. The funds are generally unrestricted, meaning recipients can allocate money as needed without stringent guidelines.

Pro Tip: Insurance Selection Strategy: Compare multiple final expense insurance quotes, carefully reviewing coverage amounts, premium costs, and potential waiting periods to identify the most comprehensive and cost-effective option for your specific financial situation.

Use this table to compare final expense insurance with other common end-of-life funding strategies:

Funding Strategy | Approval Speed | Medical Exam Required | Flexibility of Use |

Final Expense Insurance | Days to weeks | Rarely | Funds can cover any need |

Standard Life Insurance | Weeks to months | Usually required | Paid to beneficiaries |

Dedicated Savings Fund | Immediate access | Not applicable | Use determined by family |

Veteran Benefits | Weeks to months | Service required | Often restricted to burial |

Paying for Funeral and Medical Bills

Funeral and medical expenses represent two of the most significant financial challenges families face during end-of-life transitions. These costs can quickly escalate, creating substantial financial strain for surviving family members who are already navigating emotional grief and complex administrative responsibilities.

Funeral Expenses typically range from $7,000 to $12,000, encompassing a wide array of services and products. This total includes funeral home fees, casket or cremation expenses, burial plot costs, transportation, embalming, ceremony arrangements, and memorial service requirements. Families often find themselves making rapid financial decisions during an emotionally charged period, which can lead to unintended overspending or financial stress.

Medical bills present an equally challenging financial landscape. Hospitalization, specialized treatments, medication, medical equipment, and extended care services can generate overwhelming expenses. Many individuals discover that health insurance and Medicare coverage do not fully address all end-of-life medical costs, leaving families responsible for substantial out-of-pocket expenses. Final expense insurance offers a strategic solution for managing these unpredictable financial obligations, providing a financial safety net that can help mitigate the economic impact of comprehensive medical care.

Multiple funding strategies exist for managing these expenses, including dedicated savings accounts, life insurance policies, final expense insurance, veteran benefits, and potential assistance from religious or community organizations. Proactive planning and comprehensive financial research can help individuals identify the most appropriate resources for their specific circumstances, potentially reducing the financial burden on surviving family members.

Pro Tip: Financial Management Strategy: Create a comprehensive end-of-life expense folder containing insurance policies, pre-arranged funeral plans, medical directives, and a detailed inventory of potential financial resources to streamline decision-making during challenging times.

Protecting Loved Ones From Unpaid Debts

Unpaid debts can create significant financial complications for families after an individual’s passing, potentially transforming a difficult emotional period into a complex legal and financial challenge. Understanding how these financial obligations are managed becomes crucial for protecting family members from unexpected financial burdens.

When an individual passes away, their outstanding debts do not simply vanish but are instead processed through the deceased’s estate. Creditors have legal rights to seek repayment from available assets, which means the executor of the estate must systematically address these financial obligations before distributing remaining resources to beneficiaries. Debt Settlement typically follows a specific hierarchy: secured debts like mortgages and car loans are prioritized, followed by unsecured debts such as credit card balances and personal loans.

Critical protective strategies can help minimize the potential financial impact on surviving family members. These include maintaining comprehensive life insurance coverage, establishing clear estate planning documentation, and maintaining transparent communication about potential financial obligations. Some debts may be discharged entirely if insufficient assets exist to cover them, but certain types of debt - such as federal student loans or tax obligations - often cannot be eliminated through standard estate settlement processes.

Specific categories of debt require particular attention during estate planning. Joint accounts, co-signed loans, and community property state regulations can create unique scenarios where family members might unexpectedly become responsible for outstanding financial obligations. Proactive legal and financial consultation can help individuals develop strategic approaches to minimize potential debt-related risks and protect their loved ones from unexpected financial complications.

Pro Tip: Financial Protection Strategy: Conduct a comprehensive debt inventory annually, documenting all outstanding financial obligations and potential transferable debts, to create a clear roadmap for estate executors and minimize potential financial surprises for your family.

Protect Your Legacy with Trusted Final Expense Insurance Solutions

Facing the reality of end-of-life expenses can be overwhelming. From medical bills to funeral costs and outstanding debts, the financial burden can leave your loved ones under unexpected stress. This article highlights the importance of comprehensive planning that covers all critical costs while debunking common myths about coverage and expenses. If you want to safeguard your family’s future and ensure your legacy is protected, taking proactive steps today is essential.

At LD Financial Services, we specialize in helping middle-aged and senior adults navigate these challenges with compassionate, affordable final expense insurance. Our straightforward application process and fixed premiums provide peace of mind by covering funeral expenses, medical bills, and debts that might otherwise fall on your family.

Don’t wait until the last minute to prepare. Explore your options for guaranteed issue or term life policies designed to meet your unique needs. Learn more about how final expense insurance works and how it can ease the financial burden during difficult times by visiting LD Financial Services. Take control of your legacy now and book a free appointment with one of our licensed agents to get started on a personalized plan that protects those you care about the most.

Frequently Asked Questions

What are the main categories of end-of-life expenses?

End-of-life expenses primarily include medical costs, funeral and burial expenses, legal and administrative fees, and outstanding debt settlements. Understanding these categories is crucial for comprehensive financial planning.

How can final expense insurance help with end-of-life costs?

Final expense insurance provides a dedicated financial resource to cover funeral expenses and medical bills. It typically offers smaller coverage amounts and simplifies the application process, making it easier for seniors or those with health issues to obtain.

What are common myths about end-of-life expenses?

Common myths include the belief that healthcare costs dominate an individual’s final year, and that standard health insurance or government programs will cover all expenses. In reality, only 13% of personal healthcare expenditures occur in the last year of life, and many costs may not be fully covered.

How can families prepare for unpaid debts after a loved one passes away?

Families should maintain comprehensive life insurance coverage and clear estate planning documents. It’s important to communicate about financial obligations, as unpaid debts are settled through the deceased’s estate and can impact the financial well-being of surviving family members.

Recommended

Comments